Location Promotion Act – changes for investment funds and special investment funds investing in alternative investments

The German legisature introduced the Location Promotion Act (Standortfördergesetz ‒ StoFöG, Federal Law Gazette 2026 I No. 33) to strengthen the Germany’s position as a fund location in international competition. The law came into force on 10 February 2026 and, in addition to changes to investment law in the German Investment Code (Kapitalanlagegesetzbuch ‒ KAGB), also provides for tax changes in the German Investment Tax Act (Investmentsteuergesetz ‒ InvStG).

At the heart of the new rules are various simplifications for investments in alternative investments (e.g. private equity, venture capital, debt, infrastructure, renewables, etc.) via investment funds (known as “Chapter 2 funds”) and special investment funds (known as “Chapter 3 funds”). For investment funds, clearer provisions on trade tax at the fund level are intended to enhance legal certainty. In the case of special investment funds, the list of permissible investments will be broadened to allow investment in closed‑ended funds as well as in funds organised as commercial partnerships, without endangering their semi‑transparent status. We outline the key aspects of this below:

Amendments for investment funds

Direct investments

Investment funds are subject to corporation tax at a rate of 15% only on certain types of German-source income (for real estate income and certain other types of income, an additional solidarity surcharge applies). Trade tax is generally only levied in exceptional cases, namely where the investment fund actively manages its assets in an entrepreneurial manner. The thresholds in this area are somewhat more generous than those for commercial activity under general tax law, reflecting the specific characteristics of fund investments. Capital management companies usually ensure that these limits are not exceeded.

Under the Location Promotion Act, two safe harbour provisions relating to active entrepreneurial management were introduced in section 6(5a) of the Investment Tax Act. These provisions are intended to enhance legal certainty:

Granting of loans

The first safe harbour provision concerns the granting of loans to non-consumers (section 6(5a)(1) of the Investment Tax Act). The legislature has thereby resolved the previously open question for the taxation of debt funds, namely, whether granting loans should be regarded as a banking-type activity and hence as active entrepreneurial management. This is not the case. For German funds, this represents positive news. Foreign funds have already enjoyed protection in this regard, provided they did not maintain a permanent establishment in Germany.

For debt funds structured as partnerships, however, there is no change, even though, in our view, strong arguments also speak against classifying loan origination as a commercial activity in such cases (see Haisch/Bühler, Betriebs-Berater 2015, 1986, 1990 ff.; Bünning/Loff, Recht der Finanzinstrumente 2017, 42, 46). The fund industry has long and rightly called for an exemption from trade tax for alternative investment fund partnerships, similar to the sectoral exemptions for regulated funds already existing in Luxembourg and other European fund locations. Introducing such an exemption would send a strong signal in favour of Germany as a fund jurisdiction. To date, however, the legislature has not acted on this.

Holding of shares in corporations

The second safe harbour provision relates to the holding of shares in corporations, excluding only short-term trading or asset turnover (section 6(5a)( 2) of the Investment Tax Act). According to the explanatory memorandum to the law, activities such as participating in decisions on business policies, serving on supervisory boards and exercising inspection and audit rights in portfolio companies are covered (German Bundestag printed matter 21/2507, pp. 192 f.).

In parts of the market, this new rule is understood to mean that investment funds are no longer subject to the strict constraints of the Private Equity Decree (German Federal Ministry of Finance, 16 December 2003, Federal Tax Gazette, Part I, 2004, p. 40). If this interpretation prevails, closed-ended special funds under section 285 of the Investment Code could in future serve as flexible vehicles for active private equity strategies while shielding tax-sensitive investors from adverse tax consequences (such as contamination by commercial activity for tax-exempt investors or limited tax liability and filing obligations for foreign investors).

The tax authorities reportedly take a somewhat different view: they consider that the requirements of the Private Equity Decree, such as the prohibition on fund managers engaging in entrepreneurial activities in portfolio companies, should continue to apply to investment funds. For the closed-ended special funds mentioned above, this would be bad news, as it would result in a final tax burden of 30% at the level of the investment fund. Although the narrow wording of the provision and the explanatory memorandum to the law can be read in this way, the objective of promoting alternative investments is thereby missed. If this restrictive interpretation is applied, section 6(5a)(2) of the Investment Tax Act amounts merely to a clarification that was not really necessary.

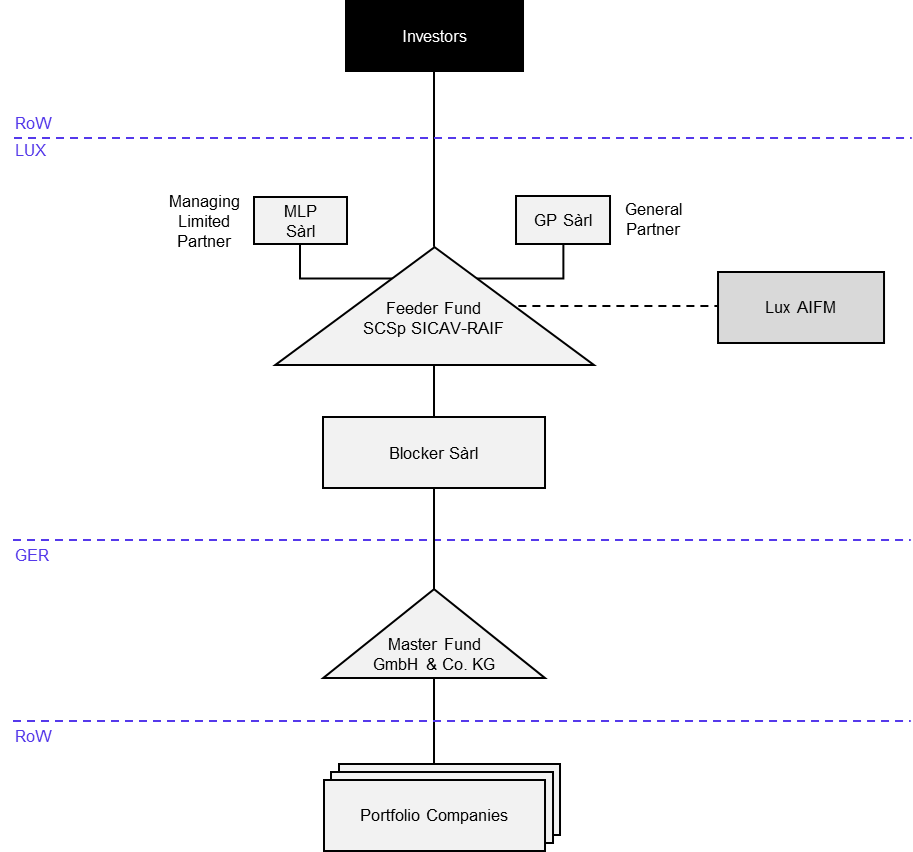

Until a genuine statutory reform is enacted, Luxembourg blocker-feeder structures, for example, a limited partnership (SCS) with a downstream blocker private limited company (Sàrl), remain the preferred access vehicle to German commercial funds for tax-sensitive investors. If the SCS is structured as an asset-managing partnership, tax-exempt investors, such as pension funds, professional pension schemes and church institutions, can invest without jeopardising their tax-exempt status. Foreign investors benefit from the fact that the blocker Sàrl shields them from German tax filing obligations. To make the structure as robust as possible from a tax perspective, an independent provider with sufficient local presence and activity should be selected.

Indirect investments via closed-end funds

With regard to indirect investments in alternative investments via closed-end funds, various reliefs have been introduced for investment funds in terms of both investment law and investment tax:

Investment law

From an investment regulatory perspective, the catalogue of eligible assets for open-ended special AIFs with fixed investment conditions pursuant to section 284 of the Investment Code has been expanded. Under section 284(2)(2)(g) of the Code, investments are now permitted not only in open-ended investment assets but also in closed-ended investment assets.

It is questionable whether the 20% limit for corporate shareholdings under section 284(3) of the Investment Code applies to investments in open-ended and now also closed-ended investment assets under section 284(2)(2)(g) of the Code. In our opinion, this is not the case because section 284(2)(2)(g) of the Investment Code constitutes an overriding special provision (see also Schmolke, in Assmann/Wallach/Zetzsche, KAGB, 1st edition 2019, § 284, para. 27; v. Livonius/Riedl, in Moritz/Klebeck/Jesch, Frankfurter Kommentar zum Kapitalanlagerecht, § 284 KAGB, para. 95).

Investment tax law

For investment tax purposes, the third safe harbour provision in section 6(5a)(3) of the Investment Tax Act is relevant to indirect investments. The new provision enables investment funds to participate directly in target funds structured as partnerships that are predominantly commercial or treated as commercial for tax purposes without this being treated as active entrepreneurial management. The prerequisite is that the investment fund demonstrates that the income derives from asset-managing activity.

Regardless of how proof is to be provided in individual cases, the new provision creates a certain degree of legal certainty. This is particularly true given that the statements in the Investment Tax Decree on passive interests in commercial partnerships were previously inconsistent (para. 6.36: prejudicial; paras. 15.39 ff.: non-prejudicial).

It should be noted that the new rule is relevant only for investments in German target funds. Investments in foreign target funds were already unproblematic before the change in law and will remain so. The reason is that active entrepreneurial management alone does not give rise to tax liability at the level of the investment fund. The management activity must also be carried out through a permanent establishment in Germany. In the case of foreign target funds, such a German permanent establishment is lacking (this view is now also reflected in the explanatory memorandum to the Location Promotion Act, German Bundestag printed matter 21/2507, p. 192).

The safe harbour provision applies only to direct interests in target funds that are predominantly commercial or treated as commercial for tax purposes. Reportedly, the tax authorities do not consider multi-tier structures involving partnerships to be covered (in our view, this interpretation is not mandatory). For fund-of-funds structures, this means the following: indirect investments via fund-of-funds in foreign target funds are (as before) unproblematic, as are indirect investments in German asset-managing target funds. Only in the case of indirect investments in German commercial partnerships, partnerships that are predominantly commercial or treated as commercial for tax purposes do taxable German-source earnings arise.

The Location Promotion Act does not change the tax treatment for investments in closed-end funds structured as corporations or in contractual form (for tax purposes: investment funds within the meaning of the Investment Tax Act). These investments have already been tax‑neutral for investment funds and remain so.

Amendments for special investment funds

The safe harbour provisions of section 6(5a) of the Investment Tax Act apply equally to special investment funds. In addition, the Location Promotion Act has introduced the following relaxations to the investment rules in section 26 of the Investment Tax Act.

Direct investments

Since the Location Promotion Act entered into force, special investment funds have been permitted to invest directly in the following assets:

Up to 100% in certain special purpose vehicles

Under section 26(6) of the Investment Tax Act, a special investment fund’s interest in a corporation must generally be below 10% of the share capital. Higher investment thresholds were previously only permitted in the case of (i) real estate companies, (ii) PPP project companies and (iii) companies whose corporate purpose is the generation of renewable energy within the meaning of section 3( 21) of the Renewable Energy Sources Act (Erneuerbare Energien Gesetz ‒ EEG). Under the Location Promotion Act, the exception to the 10% limit now also applies to interests in infrastructure project companies. In addition, for companies operating under the Renewable Energy Sources Act, the statutory definition in section 1( 19)( 6 a) of the Investment Code now applies (instead of section 3(21) of the Renewable Energy Sources Act).

Non-prejudicial income from certain active entrepreneurial management activities

As a rule, income from active entrepreneurial management must (also in future) account for less than 5% of the total income of a special investment fund. For additional electricity income, for example from photovoltaic installations and charging stations, a higher 20% threshold has applied to date.

The 20% threshold becomes obsolete under the Location Promotion Act, because, when testing compliance with the 5% limit, the following are no longer taken into account at all:

- income from managing or operating renewable energy assets within the meaning of section 1(19)(6a) of the Investment Code and from managing or operating charging stations for electromobility, in each case where this is connected with the letting and leasing of real estate;

- income from interests in real estate companies and in companies whose corporate purpose is the operation of renewable energy assets, as well as in infrastructure project companies and public–private partnership project companies; and

- income from investment units and units within the meaning of section 26(4)(h) of the Investment Tax Act, i.e. in particular private equity and venture capital funds structured as partnerships.

According to the explanatory memorandum, the intention is in particular to enable special investment funds to invest in a legally secure manner in, for example, photovoltaic installations and charging stations. In all such cases, there must always be a connection with the letting and leasing of real estate (for example, rooftop or façade installations, but also installations on covered car parks and in the immediate vicinity of the property).

Indirect investments via closed-end funds

The new section 26(4)(h) of the Investment Tax Act significantly expands the investment universe. In future, special investment funds will be permitted to invest in units of all investment assets pursuant to section 1(1) of the Investment Code, including closed-end funds structured as partnerships or corporations (German Bundestag printed matter 21/2507, 199). The previous restriction to qualified investment funds no longer applies. As a result, acquiring closed-end funds as securities within the meaning of section 26(4)(a) of the Investment Tax Act, or under the 10% de minimis threshold in section 26 of the Act, will no longer be necessary.

It has not yet been definitively clarified whether the existing exemption in the Investment Tax Decree from the 10% threshold under section 26(6) of the Investment Tax Act, which currently applies to investment funds covered by section 26(4)(h) (para. 26.37), will also extend to units in closed-end funds under the new section 26(4)(h). Given the underlying purpose of this rule ‒ to limit entrepreneurial participation by special investment funds (see German Bundestag printed matter 18/68, p. 42; 18/8045, p. 95) ‒ there are strong grounds to assume that it will. Closed-end funds do not represent entrepreneurial investments but rather passive capital investments. Nevertheless, until the Federal Ministry of Finance provides formal clarification, it is advisable to continue to keep an eye on the 10% limit as a precautionary measure.

It seems clear, however, that the exemption in the Investment Tax Decree from the 20% threshold under section 26(5) of the Investment Tax Act (para. 26.27) for investment funds also applies to units in closed-end investment funds under section 26(4)(h) as amended. This is because the Decree has never previously imposed specific requirements regarding the type of investment fund.

Temporal application

The safe harbour provisions in section 6(5a) of the Investment Tax Act apply only to financial years beginning after 9 February 2026 (section 57(11)). Accordingly, funds with a financial year that is the same as the calendar year may apply these safe harbour provisions from 1 January 2027 onwards. In the case of those whose financial year is not the same (for example, 1 November to 31 October), earlier application may be possible.

By contrast, the new investment rules for special investment funds have been in force since 10 February 2026, regardless of the fund’s financial year.

Conclusion

The Investment Promotion Act significantly improves the framework conditions for alternative investments and sends a positive signal for Germany as a fund location. The new safe harbour provisions in section 6(5a) of the Investment Tax Act provide greater legal certainty for investment funds, although their practical scope will largely depend on how the tax authorities interpret these provisions. Special investment funds stand to benefit in particular: the relaxations regarding the 10% limit for shareholdings in corporations, the 5% limit for income from active entrepreneurial management and especially the new possibilities for investing in closed-end funds, significantly broaden the investment universe.

Well

informed

Subscribe to our newsletter now to stay up to date on the latest developments.

Subscribe nowInsights